Introduction:

Pressure on companies to decarbonize their operations has dramatically increased in the past two years. With over 60% of the Fortune 500 setting ambitious goals of reaching Net Zero emissions by 2040, understanding what emissions reduction goals mean is critical to evaluating their feasibility, progress, and the company’s commitment to sustainability. In the following, Alturus will outline Scope 1, 2 and 3 emissions, how to measure each Scope, and most importantly, how to reduce each Scope emissions. The following analysis and insights were generated by the team at Alturus, with additional resources from the Environmental Protection Agency (EPA), the Greenhouse Gas Protocol, and the Science-Based Target initiative (SBTi).

Overview:

Carbon accounting has been a tool utilized by companies to calculate the impact of their operations on the environment since the 1970s. As companies began to incorporate carbon accounting into their annual reports and filings, often coupled with aggressive sustainability claims, a standard for categorizing emissions was needed. In 2001 the Green House Gas Protocol introduced the terms Scope 1, Scope 2, and Scope 3 emissions as a way of categorizing the different kinds of emissions released by a company’s operations and wider value chain. This categorization has now become the standard for emissions reporting.

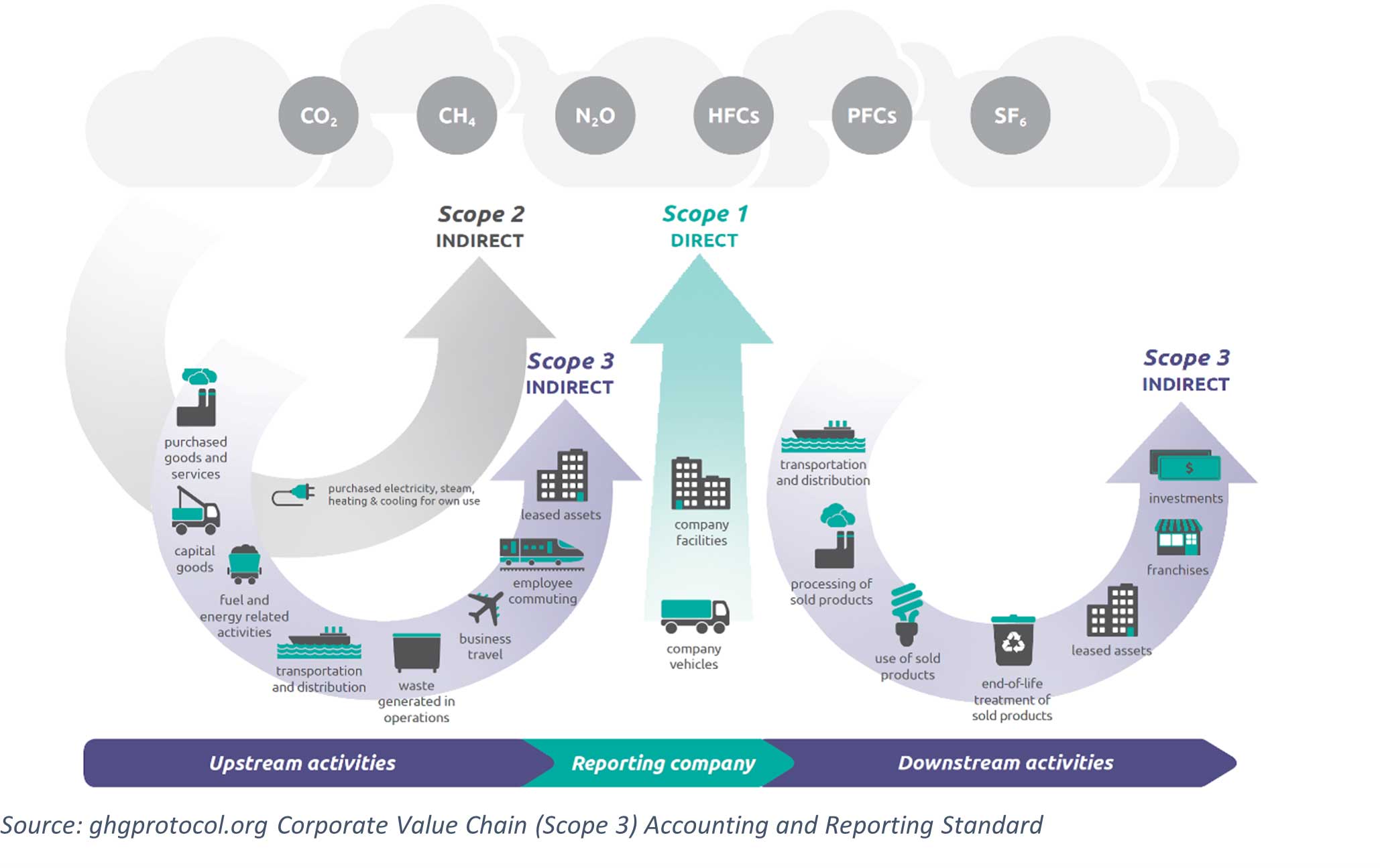

To accurately report on all emissions attributed to business operations, reporting companies must account for both direct and indirect emissions. Direct emissions are made up of Scope 1, while indirect emissions are comprised of Scope 2 and 3. A company’s total carbon footprint is the sum of each Scope of emissions, capturing a complete emissions profile. The Greenhouse Gas Protocol created the following comprehensive graphic, depicting each component of Scope 1, and Scope 2 and outlining all 15 Scope 3 categories. It has become the standard visualization of enterprise greenhouse gas emissions.

Direct:

Direct:

Direct emissions are categorized as Scope 1 and result from company owned assets and business operations. The EPA defines Scope 1 as the emissions that occur from sources that are controlled or owned by an organization (e.g., emissions associated with fuel combustion in boilers, furnaces, vehicles).

Indirect:

Where carbon accounting becomes more complicated is when indirect emissions must be measured. Indirect emissions are comprised of Scope 2 and Scope 3 emissions and do not necessarily originate at the reporting companies’ facility. Scope 2 emissions are emissions associated with the purchase of electricity, steam, heat, or cooling. Even though these emissions originate at the facility where the utility was purchased, they are accounted for in the reporting companies emissions report because they resulted from the reporting company’s operation.

The other component of indirect emissions are emissions associated with the company’s value chain; these are categorized as Scope 3. Often making up over 70% of a company’s entire emission profile, Scope 3 emissions are not only the most difficult to reduce but also the most difficult to quantify. Scope 3 emissions result from activities related to a company’s upstream and downstream value chain. Upstream Scope 3 emissions put simply are the reporting companies’ supplier’s Scope 1 and 2 emissions. Downstream Scope 3 emissions result from the use of sold products, processing of sold products, transportation of sold products and the product end-of-life treatment.

Scope 3 emission are compartmentalized into 15 categories. This helps companies better target, manage, and understand their impact. The categorization follows:

|

Scope 3 Emissions |

||||||

|

Upstream |

Category 1: Purchased goods and services |

|||||

|

Category 2: Capital goods |

||||||

|

Category 3: Fuel and energy related activities not included in Scope 1 and 2 |

||||||

|

Category 4: Upstream transportation and distribution |

||||||

|

Category 5: Waste generated in operations |

||||||

|

Category 6: Business travel |

||||||

|

Category 7: Employee commuting |

||||||

|

Category 8: Upstream leased assets |

||||||

|

Downstream |

Category 9: Downstream transportation and distribution |

|||||

|

Category 10: Processing of sold products |

||||||

|

Category 11: Use of sold products |

||||||

|

Category 12: End-of-life treatment of sold products |

||||||

|

Category 13: Downstream leased assets |

||||||

|

Category 14: Franchises |

||||||

|

Category 15: Investments |

||||||

Scope 1 Break Down:

Definition:

Scope 1 emissions are generally the easiest to measure and most common Scope referred to in stated emissions reduction goals. Scope 1 emissions are generated directly by the reporting companies owned assets, comprised of owned buildings and vehicles. Each aspect of owned facility (on-site) fuel combustion, which can power lighting, heating and cooling, and the complexities of the production process, are included in an owned facility’s emission profile. Similarly, every emission resulting from vehicles owned by the reporting company completes the Scope 1 footprint.

Measurement:

Measuring enterprise Scope 1 emissions is simpler then measuring Scope 2 and 3 emissions, yet still has its complexities. The best place to start is implementing energy usage metering throughout the reporting company’s facility footprint. Metering is an effective tool in quantifying energy usage throughout a facility. Metering equipment provides real time energy usage data which can be used to generate a report on emissions data, as well as progress on emissions reduction projects if energy conservation measures are implemented.

If metering is not available, the quickest way to determine Scope 1 emissions attributed to facilities is to quantify all fuel sources consumed onsite. Purchasing and Energy Procurement teams generally have this level of information, and once it is collected the Green House Gas Protocol as well as the EPA offers free tools to calculate the emissions profile attributed to the consumed fuel.

Comprising an inventory of enterprise owned vehicles is the simplest way to quantify Scope 1 emissions attributed to vehicle assets. After this inventory is collected, multiplying the amount of fuel these vehicles consume over the reporting period, by the emissions factor attributed to the fuel source will generate their Scope 1 emissions. Fuel source emissions factors can be found using a tool like the EPA Emissions Equivalency Calculator or on the Greenhouse Gas Protocol website.

Reduction Strategies:

Now that a Scope 1 emissions profile is generated, reducing these emissions is done through equipment upgrades, electrification, and fleet conversion. To reduce facility emissions, facility teams must reduce the amount of fuel consumed onsite. Projects with the greatest success include boiler electrification or conversion to renewable fuels, installation of combined heat and power systems, utilization of renewable thermal technologies. Converting enterprise vehicles to electric vehicles, optimizing routes, and reducing fleet size are the best ways to lower emissions attributed to vehicle assets.

Scope 2 Break Down:

Definition:

Scope 2 emissions are indirect emissions which result from the purchase of energy from a utility. This means that the emissions do not take place at the reporting company’s owned facility, rather at the point of generation. Scope 2 emissions are another common reduction goal and are largely dependent on the cleanliness of the grid.

Measurement:

Scope 2 emissions are calculated using location-based or market-based methods. Both methodologies rely on emissions factors to determine the resulting emissions. An emissions factor is a representative value, usually quantified as the weight of pollutant divided by the unit of the activity emitting the pollutant (e.g., kilograms of particulate emitted per megagram of coal burned). This emissions factor generates an estimate on the quantity of pollutant released into the atmosphere per associated energy consuming activity.

Location-based methodology involves using the average emissions intensity of the grid in which the energy is consumed. The grid’s reliance on renewable or fossil fuels greatly influences the grid’s emissions factors; the cleaner the grid, the lower the emissions factor will be. Data on grid-average emissions factors can be found for specific regions on the EPA and Greenhouse Gas Protocol websites.

Calculating Scope 2 emissions using a market-based method is more complex, and involves contractual instruments involved in the purchase of power. According to the Greenhouse Gas Protocol, “A market-based method reflects emissions from electricity that companies have purposefully chosen (or their lack of choice). It derives emission factors from contractual instruments, which include any type of contract between two parties for the sale and purchase of energy bundled with attributes about the energy generation, or for unbundled attribute claims. Markets differ as to what contractual instruments are commonly available or used by companies to purchase energy or claim specific attributes about it, but they can include energy attribute certificates (RECs, GOs, etc.), direct contracts (for both low-carbon, renewable, or fossil fuel generation), supplier-specific emission rates, and other default emission factors representing the untracked or unclaimed energy and emissions (termed the residual mix) if a company does not have other contractual information that meets the Scope 2 Quality Criteria”.

Reduction Strategies:

Scope 2 emissions are reduced by decreasing the reliance on purchased power from utilities or third parties. This can be done by implementing energy conservation measures at energy intensive facilities. Energy conservation measures will not only generate emissions reductions (lowering Scope 1, and 2) but can also drive down energy costs, which will lower operating expenses. Evaluating and implementing on-site generation of renewable power is another effective strategy. In grids which are heavily reliant on fossil-fuels, on-site renewables coupled with battery storage can provide the facility with clean power when it needs it most. If on-site generation is not an option, virtual power-purchase agreements (VPPA) can also materially drive down Scope 2 emissions. Through a VPPA, the reporting company acquires renewable energy certificates from a specific renewable energy project developer.

To Reduce Scope 2 emissions Alturus evaluates for and implements, on-site renewable generation projects, alternative fuel sourcing for thermal, VPPAs, and thermal REC options. The team at Alturus is responsible for over 1.4GW of VPPA for 1/4 of the leading Fortune 500 Companies.

Scope 3 Breakdown:

Definition:

Scope 3 emissions, on average, make up over 70% of total enterprise emissions, are the hardest to reduce, and involve long-term and complex reduction goals. Distributed amongst 15 categories, Scope 3 emissions are comprised of upstream (Category 1-8) and downstream (Category 9-15) activities. The separation of upstream and downstream Scope 3 emissions is crucial to understanding and quantifying a Scope 3 profile.

Upstream Scope 3 emissions are indirect emissions which result mainly from the reporting company purchasing goods and services (Category 1,2,4). The emissions which result from the manufacturing, transportation, and distribution of these goods (the reporting company’s upstream supply chain) are attributed to the reporting company’s Scope 3 emissions. Upstream Scope 3 emissions also include employee commuting and business travel (Category 6,7). Employee transportation and business travel only results in Scope 3 emissions if employees are traveling in vehicles owned by a 3rd party.

Downstream Scope 3 emissions are indirect emissions which result from distribution (Category 9), processing (Category 10), product use (Category 11), and end-of-life treatment (Category 12) of goods and services sold by the reporting company. Also included in downstream Scope 3 emissions are investments made by the reporting company (Category 15). This category mainly applies to financial institutions and is easily mitigated by shifting investment from historically dirty sources (fossil fuels, construction, transportation) to greener, more environmentally friendly alternatives.

Measurement:

Measuring upstream emissions is incredibly difficult and involves transparency between the reporting company and its supply chain. Estimations on the required energy spend per product purchased are often relied on to calculate the upstream effects of purchased goods. These estimations can then be used to identify which purchased goods are the most energy intensive. To estimate emissions which result from the distribution of purchased goods, employee commuting and business travel, the reporting company can rely on activity-based data. This is a more precise measurement utilizing the time, distance, and fuel type used to transport purchased goods, and employees. If the reporting company has a transparent relationship with its supply chain, collecting and calculating this information can be much easier. However, energy intensity per unit produced is often a market tool to determine product price and can be difficult to obtain in even the clearest business relationships.

Reporting companies have a relatively easier time accounting for downstream Scope 3 emissions. Since these emissions result indirectly from the purchase of their goods and services, companies can calculate the life-time emissions of their products (if applicable), estimate the emissions required to recycle and process their products and, using the same activity-based data as upstream emissions, estimate the emissions which result in the transportation and distribution of their sold product.

Reduction Strategies:

The main strategy for reducing enterprise Scope 3 emissions is through supplier engagement, and operational policy and procurement choices. Using the resource: Value Change in the Value Chain: Best Practices in Scope 3 Greenhouse Gas Management from the SBTi and Alturus’ project experience, the following table outlines the most successful mechanisms for reducing upstream and downstream Scope 3 emissions.

|

Scope 3 Emissions Reduction Strategies |

||||||

|

Upstream |

Category 1: Purchased goods and services |

Engaging with suppliers on aligning sustainability initiatives while making procurement choices based on sustainability performance is an effective way to influence supplier decarbonization. This can be done through supplier portals and publicly announced supply chain decarbonization initiatives, which encourage supplier participation. Additionally, innovative solutions in product design which reduce the need of energy intensive goods and services can significantly decrease Category 1 emissions. |

||||

|

Category 2: Capital goods |

Like Category 1, reducing Category 2 requires supplier engagement through a portal or a supplier decarbonization initiative which rewards sustainable performance. However, there is more opportunity in reducing Category 2 emissions with sustainable product design. |

|||||

|

Category 3: Fuel and energy related activities not included in Scope 1 and 2 |

Most Category 3 emissions result from the mining of coal, refining of gasoline, transmission and distribution of natural gas, production of biofuels as well as emissions which occur in the loss of fuel during transportation (leaks). To mitigate these emissions the reporting company can procure fuel from renewable/clean sources and procure fuel with short transmission and distribution system to mitigate loss. |

|||||

|

Category 4: Upstream transportation/ distribution |

Purchasing products from local suppliers while optimizing supply routes can reduce Category 4 emissions. The shorter the distance purchased goods and services need to travel, the lower the emissions. |

|||||

|

Category 5: Waste generated in operations |

Decreasing the amount of waste produced in the product manufacturing process reduces Category 5 emissions. This is accomplished through increased recycling efforts, sustainable product design, wastewater efficiency initiatives and landfill mitigation strategies. |

|||||

|

Category 6: Business travel |

Optimizing employee travel to minimize unnecessary or long-distance trips. Exploring alternatives to air travel and when possible, utilizing virtual meetings. |

|||||

|

Category 7: Employee commuting |

Establishing a corporate ride share or carpool program (optimally with electric vehicles) is the most efficient way to decarbonize employee commuting. If a corporate transportation system is not available, promoting and encouraging public transportation is effective as well. |

|||||

|

Category 8: Upstream leased assets |

This category is applicable only to companies that operate leased assets. If leased assets are part of the business model, integrate sustainable procurement choices when assessing opportunities. |

|||||

|

Down stream |

Category 9: Downstream transportation/ distribution |

Decreasing Category 9 emissions relies on product design, distribution center efficiency, and supply routes. In general, it is more efficient to transport lighter products, and if coupled with route optimization Category 9 emissions can decrease substantially. Owning and operating distribution centers also shifts the attributed emissions from Scope 3 to Scope 1, and 2. Then traditional energy conservation measures can be deployed to lower absolute emissions. |

||||

|

Category 10: Processing of sold products |

If products must be processed before use, then engagement with end customers is an effective way to reduce Category 10 emissions. Teaching end customers the most efficient and effective ways to process products can also help in reducing emissions associated with Category 12. |

|||||

|

Category 11: Use of sold products |

Reducing Category 11 emissions requires designing energy efficient products and engaging with end customers on the most efficient use. |

|||||

|

Category 12: End-of-life treatment of sold products |

Reducing packaging materials while increasing recyclability of products will reduce Category 12 emissions. Engaging with customers on the proper end-of-life product treatment and finding innovative ways to incorporate recycled products back into the manufacturing process has had recent success in multiple sectors. |

|||||

|

Category 13: Downstream leased assets |

This category is applicable only to companies that operate leased assets. If leased assets are part of the business model, integrate sustainable procurement choices when assessing opportunities. |

|||||

|

Category 14: Franchises |

Only applicable to franchisors, ensuring leased facilities are as energy efficient as possible (i.e. Scope 1 and Scope 2 emission reductions) |

|||||

|

Category 15: Investments |

Applicable to financial institutions, integrating a sustainable investment strategy while divesting from traditionally dirty markets generates Category 15 reductions and can even provide more secure investments. |

|||||

About Alturus:

Alturus provides strategic decarbonization services to the world’s largest energy users. Alturus identifies, implements and funds decarbonization projects which generate material energy, cost, and emissions reductions from day one. An innovative end-to-end solution, Alturus’ decarbonization programs achieve corporate sustainability goals ahead of schedule with no upfront cost by the Customer or its suppliers.

As an EaaS solution, Alturus achieves absolute emission reductions enterprise-wide, at scale. Our Scope 1, 2 and 3 programs are fully funded by Alturus’ balance sheet which covers all project development, construction, and maintenance costs.

To learn how Alturus can achieve absolute emissions reductions across your entire enterprise reach out to a member of our team at info@alturus.com

For more information on Alturus and our decarbonization solutions visit our Solutions page at www.alturus.com/solutions/

To explore our international project portfolio, visit www.alturus.com/project-portfolio/